Even if you’ve been filling out Form 1040 and any other associated forms and schedules for years, things will be different this filing season.

This is the first year we taxpayers (and tax pros) will be filing under the extensive new Tax Cuts and Jobs Act (TCJA) changes.

In addition to new tax rates and deduction amounts, there are a variety of other tax law tweaks that could affect what goes on — or now doesn’t — your Form 1040, which itself is new.

So before you start working with your tax preparer or open up your tax software, either the package you bought or downloaded or are using via Free File (yes, it’s already open), here are some things to think about and documents that you might need to do the job.

Start with last year: Tax laws have changed, but your 2017 filing is still the best place to start. This includes not only your federal forms, but also your prior year’s state tax filing if you live in a state that collects an income tax.

If your personal and financial life didn’t change much in 2017, your previous return will give you a good idea of what to expect this time round even if the way the new tax laws treat your situation is a bit different.

Plus, these documents will have some data, such as Social Security numbers and bank account info if you’re have your refund directly deposited, that you’ll need again this year.

Perennial filing documents: The world, including the Internal Revenue Service, largely has gone digital. That should help you in the gathering of the tax and financial documents that you’ll need to fill out your taxes.

Most third-party tax reporters — these are the folks that let you and the IRS know how much money you made at your job, either full-time or as a freelancer, and how much unearned income you got from investments — must get you this relevant income info by Jan. 31.

Some documents, however, come sooner, especially if you’ve opted to receive this data electronically. Check your email inbox and accounts for this data, then download it a special tax filing folder.

Among the documents you of particular tax-filing note are:

· W-2 forms reporting your wages and W-2G for gambling winnings if you had a really good time in Las Vegas,

· Various 1099s with sundry income amounts, including 1099-R for retirement; 1099-INT for interest earned; 1099-DIV for investment dividends; 1099-B for brokerage sales; 1099-G for unemployment benefits, state tax refunds or other government payments; and 1099-MISC for independent contractor and other types of, as the extension indicates, miscellaneous income, and

· Some 1098s, such as 1098-T that students will need to calculate education tax credit eligibility; 1098-E with potentially deductible student loan interest payment amounts; or the plain old Form 1098 for homeowners with mortgage interest, loan points and, in some cases, payments made toward private mortgage insurance real estate taxes.

More specialized filing material: Every filer’s tax situation is unique. That’s why you could need additional information that applies to your financial circumstances and tax-filing needs.

Considerations here include:

· Records of estimated tax payments you made for both your federal and state taxes.

· Do you get tips or other gratuities as part of your job? Have your records of those payments handy.

· Were you unemployed for a bit? The W-2G you got is income that has to be included on your 1040, just like with the gambling and prize winnings mentioned earlier.

· For the 2018 tax year, if you got alimony, that’s taxable income. If, however, you paid alimony, it’s an adjustment to your income, aka an above-the-line deduction. In these cases, the income and deductibilty considerations are grandfathered in despite TCJA changes to these divorce matters that start in 2019.

· Did you move for a job last year? Sorry, you probably aren’t going to be able to count on Uncle Sam to help cover your relocation costs. This above-the-line deduction and the associated income exclusion for workers whose new employers pay relocation costs, now is available only to members of the Armed Forces.

· Distributions from retirement accounts, depending on the type of plan you have, could be taxable. Double check income statements for your workplace retirement and/or IRA withdrawals, as well as your Social Security benefits if you’re now getting those payments.

· If you’re still contributing to your retirement plan, is any of it deductible? Have your statement of these amounts to help you decide.

A few more questions: In addition to collecting all your filing material, take the time to answer a few questions that could have tax implications. They include:

Do you have any unresolved state or IRS tax issues?

Did you get married or divorced last year? This will affect, among other things, your filing status.

Are you supporting anyone not living with you?

Did you have a child last year? Was that new family addition adopted or the adoption process begun last year?

Did you pay for a dependent child‘s (or another dependent’s) care so you could go to work?

Did you receive any assistance from your employer to pay for education expenses, child care costs or adoption expenses?

Did you or any member of your household pay any college costs?

Did you hire household help?

Did you make any major improvements to your home?

Did you sell, refinance or face any foreclosure transactions on your personal residence?

Do you own a second residence or any other real estate? If so, did you rent it out last year?

Were you a resident of, or did you have income in, more than one state during the year?

Did you have money in a foreign account?

Did you make any large purchases, such as a vehicle?

Did you have any nonresidential debt that was canceled?

Did you serve in the military? If so, did you receive combat pay?

Did you have health care coverage? Did you buy your medical insurance through the market place?

Which deduction method do you plan to use, claiming the standard amount for your filing status or itemizing?

Affordable Care Act still applies: Maybe all the talk by the White House and Republicans on Capitol Hill has you wondering about that health care question in the above list.

The short answer is that for your 2018 tax return, tax requirements involving Obamacare as it’s popularly known are still in effect and the IRS will continue to enforce the tax components.

So for this filing season, unless you qualify for an exemption, you must continue to report your health care coverage or pay the individual shared responsibility payment for tax year 2018.

For planning purposes, the individual mandate is repealed effective this year, meaning you won’t have to pay the added tax if you choose to go without health insurance this and future years.

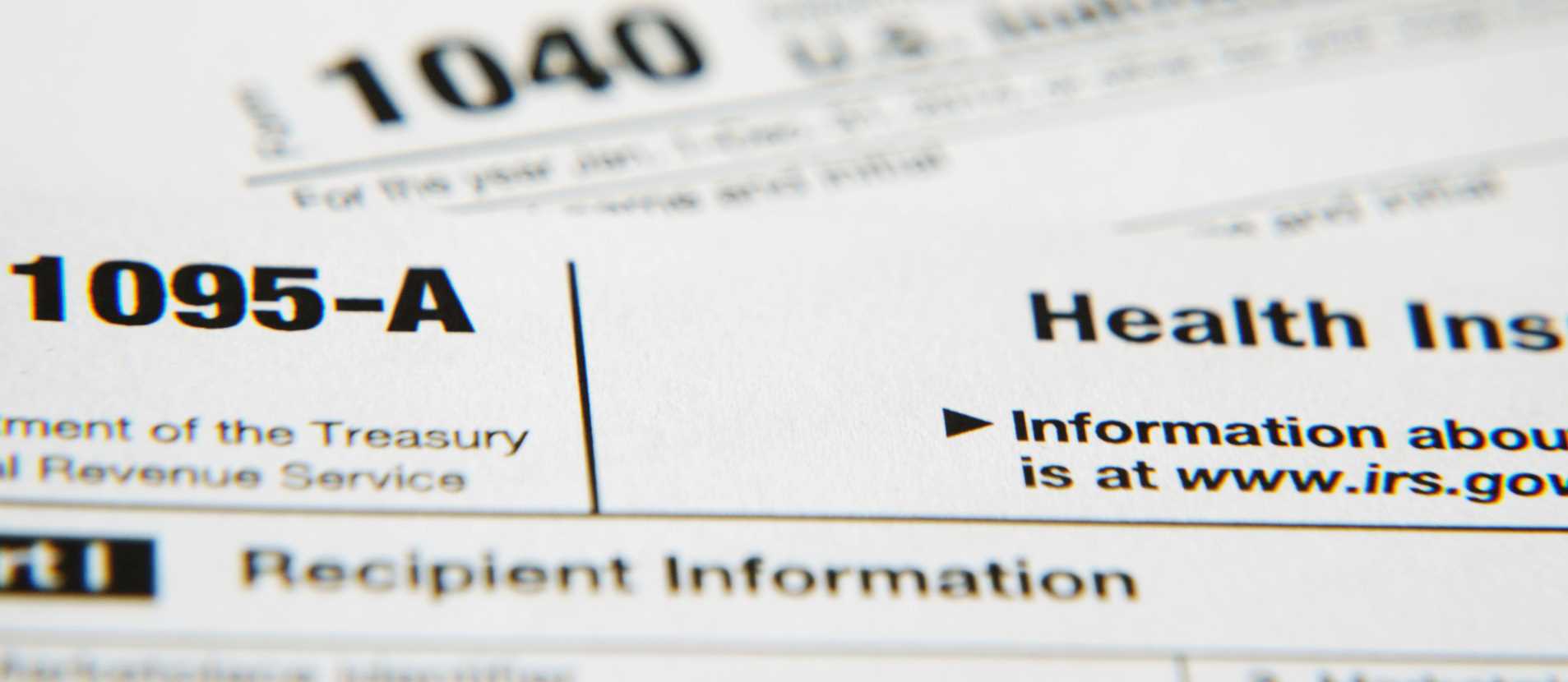

But back to the here-and now. For your 2018 return, you should be on the lookout for Obamacare-related tax forms:

· Form 1095-A is officially titled the Health Insurance Marketplace Statement. As the name indicates, it is sent by the exchanges through which individuals purchased their medical coverage.

· Form 1095-B is issued by health care insurance issuers or some smaller companies that provide coverage for employees, confirms that you had at your workplace acceptable minimal health insurance coverage. It also shows how long you were covered and which family members also were on your policy.

· Form 1095-C is the same as the 1095-B, but it is issued by large employers.

The B and C 1095s generally will mean you just have to check a box on Form 1040 to let the IRS know that you had health care coverage and therefore don’t owe a tax penalty.

The A version of 1095 is key if you’re eligible for the premium tax credit, also known as the federal subsidy, to help you pay for your ACA-mandated coverage that you got through the marketplace.

Schedule A specific information: Now for folks who answered “itemizing” to the deduction method question. This choice could have a major impact on the filing documents you need.

The TCJA almost doubled the standard deduction amounts, so more taxpayers are expected to use this easier-to-claim deduction method this (and future) filing seasons.

But if you do find that itemizing still works better for you (and some of us still do), take note of the new law’s Schedule A changes and what you now need (or won’t need) to complete it.

Here’s a breakdown, using the new Schedule A as a guide, of what’s still deductible and what you need to claim the expenses.

Medical

These expenses survived the first major tax reform in more than 30 years. In fact, for the 2018 tax year, they were enhanced. You still can claim allowable doctor, dentist and a URL variety of health care related costs and this filing season they only have to exceed 7.5 percent of your adjusted gross income (AGI). For the 2019 tax year, though, you’ll have to meet 10 percent of AGI when you file those returns in 2020.

Regardless of the tax year, if you claim medical costs you’ll need records of your expenditures, not to submit but in case the IRS questions the claims. This includes prescriptions, doctor office visit payments, dental care costs, hospital bills, medical insurance premiums as long as they aren’t paid at work via pretax dollars, long-term care insurance premiums and the mileage to and from physicians’ offices.

State and local taxes (SALT)

This component of the “Taxes You Paid” section of Schedule A didn’t fare as well under TCJA. You still can claim the taxes you paid to your state and local tax collectors, including income or sales taxes — remember, can’t deduct both; you must choose sales or income taxes to claim — along with real estate and personal property taxes, but there’s now a limit. Only $10,000 can be counted here. For most folks not living in high-tax states or expensive neighborhoods, this shouldn’t be a problem. And if you’re not near the 10 grand cap and are claiming sales taxes, don’t forget about adding in sales tax that was tacked on to a major purchase, such as a car, boat or airplane.

Your state and local officials should provide you with receipts or similar documents detailing the taxes you can claim. If you want to add up your sales taxes yourself rather than use the optional state sales tax table amounts the IRS provides in the Schedule A instructions, you’ll need all those receipts, too.

Interest

This mainly applies to homeowners, who still can claim the deductible interest on their mortgage. This will be reported on the previously mentioned Form 1098 or an IRS acceptable substitute document.

Note, however, that the limit on the amount of home loan on which you can claim this deduction was reduced under the new tax law. Instead of interest on home indebtedness up to $1 million, you now can deduct only the interest on home loan amounts up to $750,000. Don’t panic, though, if you have an older, larger home mortgage. If you got the loan on or before Dec. 15, 2017, your itemized mortgage interest claim is grandfathered in at the prior $1 million level.

One area, however, where more folks might take a deduction hit is with interest on home equity loans or home equity lines of credit (HELOC). These used to be fully deductible. Under TCJA, however, no matter when you got such a home-secured debt, the interest cannot be claimed if the proceeds were used for something else, say to pay your children’s college tuition. This loan interest now is deductible only when the loan or HELOC proceeds are used to buy, build or improve the property used to secure the loan.

And because of Congressional inaction, not TCJA revisions, the option to claim any private mortgage interest (PMI) premiums is gone. It’s possible that the House and Senate could get to this and other so-called extenders, but not probable that it will do so soon. Lawmakers belatedly renewed this and a couple of other expired laws for the 2017 tax year in February 2018. If PMI makes a difference in your decision to itemize, you might want to consider delaying your filing to see if this becomes available later in the filing season.

Charitable gifts

This itemized deduction is still on Schedule A and you can even give more that before if you’re able because the deduction limit for gifts to public charities is increased from 50 percent to 60 percent of AGI. But you still need to follow the other rules, like getting contemporaneous substantiation — a receipt — for any contribution of $250 or more. In fact, get receipts from all the nonprofits to which you give regardless of how large or small your donation.

And since donation deductions still must be claimed as an itemized expenses, many folks are looking at other tax-related philanthropic strategies.

Casualty and theft losses

This section is still on Schedule A, but now also is more restricted. You can only claim losses related to a federally declared disaster. In addition to the documentation of the losses and expenses not paid by insurance toward recovery, you’ll also have to include the Federal Emergency Management Agency (FEMA) number and the location of property against which the tax claim is being made.

Other itemized deductions

This section for reporting specific itemized deductions gets a lot of attention because it’s where you enter your gambling losses. This includes, among other things, the cost of losing bingo, lottery and raffle tickets, horse and dog racing slips and the money you dropped at the poker table or roulette wheel at your favorite casino. Obviously, you’ll need to keep good track of these expenditures. Remember, though, that your losses can only offset the amount of winnings you got during the tax year, some of which were on the W-2G form mentioned earlier. You can’t claim losses to produce a loss on your taxes.

Miscellaneous no more: Thanks to some key TCJA changes, the records you need to file have been reduced. Of course, that means your chance to use these areas to trim your tax bill also is gone.

Long-time itemizers probably noticed in the above discussion of Schedule A that somethings missing. I’m talking about miscellaneous itemized deductions section

This means you no longer have to keep track of documentation for such previously deductible (as long as the total exceeded 2 percent of your AGI) expenses as miscellaneous deductions. This section was eliminated by the TCJA. That means no more bothering with receipts for unreimbursed job expenses, expenditures on searching for a new job, hobby costs, various investment expenses and tax preparation fees.

Whew! That’s a lot of stuff to consider regardless of whether you use Schedule A or take the easier standard deduction route.

And it’s a lot of material for you to get together, either to file your taxes yourself or deliver to your tax preparer.

With the official start of tax filing season 2019 just days away (official opening is Jan. 28), it’s time to get started tracking down these documents so you can be done with your taxes as soon as possible.

KAY BELL